While it’s easy to see today how Environmental, Social, and Governance (ESG) Reporting is crucial to an organization’s performance and accountability, it’s important to understand how the sustainability landscape has evolved into what it is today.

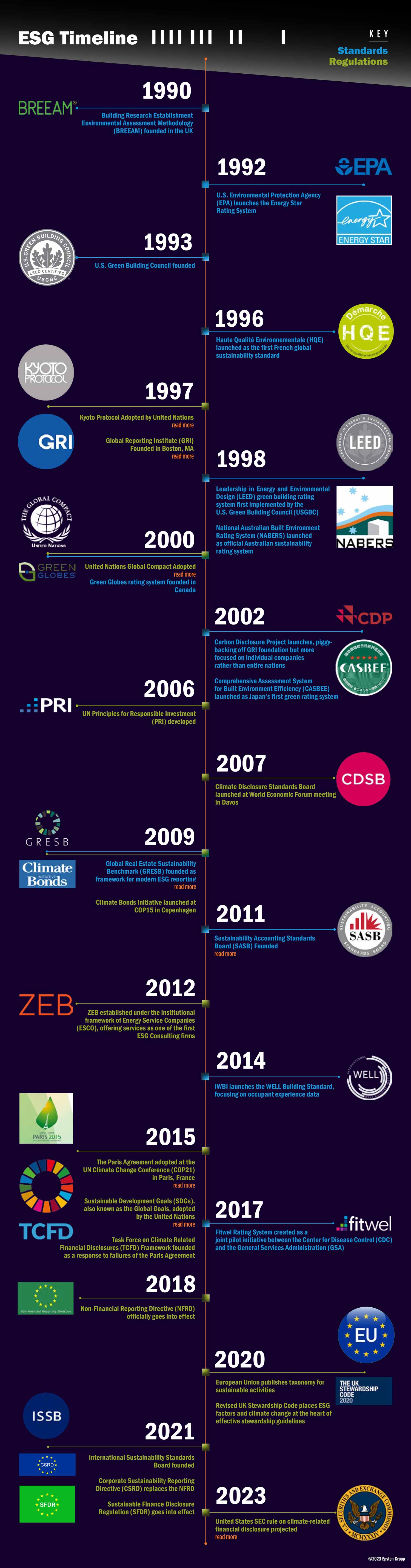

Kyoto Protocol Adopted by United Nations

The Kyoto Protocol, adopted by the United Nations (UN) in 1997, is a treaty aimed at combating climate change by encouraging the reduction of carbon emissions worldwide. The Protocol is based on a consensus among the scientific community that global warming is primarily caused by carbon emissions made by human activities.

Through the Protocol, 37 nations voluntarily pledged to reduce their greenhouse gas emissions. It placed the burden for emission reductions primarily on developed nations, viewing them as largely responsible for the industrialized effects of climate change.

While The Kyoto Protocol would later be replaced by the 2015 Paris Climate Accord, it marked a historic moment in the effort against climate change by acknowledging, on an international scale, that there existed a collective responsibility to mitigate human impacts on the environment.

Global Reporting Institute (GRI) Founded in Boston, MA

The Global Reporting Institute (GRI) was founded in Boston, Massachusetts in 1997, following the adoption of the Kyoto Protocol and public outcry over the environmental damage of the Exxon Valdez oil spill. It aimed to create an accountability mechanism to ensure companies adhered to responsible environmental conduct. The first version of what was then the GRI Guidelines (G1) coalesced economic, social, and governance issues into a global sustainability reporting framework.

In 2016, GRI transitioned from providing guidelines to setting the first global standards for sustainability reporting – the GRI Standards. The Standards continue to be updated and added to today, maintaining GRI’s historic reputation as pioneers in the field of ESG Reporting.

United Nations Global Compact Adopted

Introduced in 2022 as a non-binding pact, The United Nations Global Compact aims at encouraging businesses and firms worldwide to adopt sustainable and socially responsible policies. The Compact introduced a landmark goal that includes reporting the results of these policies.

The Compact is governed by its Ten Principles, which require that organizations are “operating in ways that, at a minimum, meet fundamental responsibilities in the areas of human rights, [labor], environment and anti-corruption.” The Compact relies on “public accountability, transparency, and enlightened self-interest.”

Though it does not mandate compliance, the Compact was the first time widespread participation of massive corporations was seen making efforts towards a more just world. Several major organizations signed the compact following its adoption, including BP, Danone, Deloitte Touche, GAP, HSBC, ICI, Nestlé, Nike, and Tata.

Global Real Estate Sustainability Benchmark founded as framework for modern ESG reporting

Prior to the founding of the Global Real Estate Sustainability Benchmark (GRESB) in 2009, no systematic information on the environmental performance of public and private real estate investments existed.

After its founding, real estate investors and stakeholders were able to look to a portfolio’s GRESB score (a percentage from 0 to 100) to guide responsible investments.

Sustainability Accounting Standards Board (SASB) Founded

The Sustainability Accounting Standards Board (SASB) was founded as a nonprofit organization to help businesses and investors develop a common language around the financial impacts of sustainability. As the landscape surrounding ESG reporting continued to evolve and more organizations grew interested in participating, it was necessary to establish standardization of these reporting processes.

SASB’s mission “is to establish industry-specific disclosure standards across ESG topics that facilitate communication between companies and investors about financially material, decision-useful information. Such information should be relevant, reliable and comparable across companies on a global basis.”

The Paris Climate Accord adopted at the UN Climate Change Conference (COP21) in Paris, France

The Paris Agreement is an international treaty on climate change adopted by 196 Parties at the UN Climate Change Conference (COP21) in Paris, France, on December 12, 2015. It entered into effect on 4 November 2016 with an overarching goal to hold “the increase in the global average temperature to well below 2°C above pre-industrial levels” and pursue efforts “to limit the temperature increase to 1.5°C above pre-industrial levels.”

The Agreement works on a five-year cycle of increasingly ambitious climate action plans, known as nationally determined contributions (NDCs). Each successive NDC is meant to reflect an increasingly higher degree of ambition year over year.

Sustainable Development Goals (SDGs), also known as the Global Goals, adopted by the United Nations

The Sustainable Development Goals (SDGs), also known as the Global Goals, were adopted by the UN in 2015 as a universal call to action to end poverty, protect the planet, and ensure that by 2030, all people enjoy peace and prosperity. The 17 SDGs recognize that action in one area will affect outcomes in others, and that development must balance social, economic, and environmental sustainability.

These goals offer a framework for ESG mapping at a higher level. They can help to increase the adoption of sustainable investing, encourage responsible corporate behavior, and integrate sector and business specific ESG factors with broader social issues and global environmental goals.

United States SEC rule on climate-related financial disclosure projected for April

In 2022, the U.S. Securities and Exchange Commission (SEC) published a proposed rule requiring publicly traded companies to report on climate-related risks. The Enhancement and Standardization of Climate-Related Disclosures for Investors drew a wide differing range of resistance and support in over 15,000 comments. The SEC has indicated that it plans to finalize the rule in 2023.

Knowing where we came from helps us look more clearly ahead, and in the case of ESG Reporting, the future of the practice is fast approaching. If you are interested in beginning your journey with ESG, reach out to us; we’ll meet you wherever you are.